import math

from dataclasses import dataclass

import joypy

import matplotlib.pyplot as plt

import numpy as np

import pandas as pd

from matplotlib import cm

from tqdm import tqdm

@dataclass

class CIRProcess:

"""An engine for generating sample paths of the Cox-Ingersoll-Ross process"""

kappa: float

theta: float

sigma: float

step_size: float

total_time: float

r_0: float

def generate_paths(self, paths: int):

"""Generate sample paths"""

num_steps = int(self.total_time / self.step_size)

dz = np.random.standard_normal((paths, num_steps))

r_t = np.zeros((paths, num_steps))

zero_vector = np.full(paths, self.r_0)

prev_r = zero_vector

for i in range(num_steps):

r_t[:, i] = (

prev_r

+ self.kappa * np.subtract(self.theta, prev_r) * self.step_size

+ self.sigma

* np.sqrt(np.abs(prev_r))

* math.sqrt(self.step_size)

* dz[:, i]

)

prev_r = r_t[:, i]

return r_tShort rate dynamics: mean and variance

The short rate under the CIR model has the dynamics:

\[dr_t = \kappa (\theta - r_t)dt + \sigma \sqrt{r_t}dB_t\]

For a moment, if we drop the stochastic term, and merely consider the first order linear ODE \(\frac{dr_t}{dt} + \kappa r_t = \kappa \theta\), the integrating factor for this differential equation is \(e^{\int \kappa dt} = e^{\kappa t}\). Multiplying both sides by the integrating factor, we have:

\[\begin{align*} e^{\kappa t} dr_t &= \kappa(\theta - r_t) e^{\kappa t}dt + \sigma e^{\kappa t}\sqrt{r_t} dB_t \\ e^{\kappa t} dr_t + r_t e^{\kappa t}dt &= \kappa e^{\kappa t}\theta dt + \sigma e^{\kappa t}\sqrt{r_t} dB_t \\ d(e^{\kappa t} r_t) &= \kappa e^{\kappa t}\theta dt + \sigma e^{\kappa t}\sqrt{r_t} dB_t \\ \int_{0}^{t} d(e^{\kappa s} r_s) &= \theta \kappa\int_{0}^{t} e^{\kappa s} ds + \sigma \int_{0}^{t} e^{\kappa s}\sqrt{r_s} dB_s \\ [e^{\kappa s} r_s]_{0}^{t} &= \kappa \theta \left[\frac{e^{\kappa s}}{\kappa}\right]_{0}^{t} + \sigma \int_{0}^{t} e^{\kappa s}\sqrt{r_s} dB_s\\ e^{\kappa t}r_t - r_0 &= \theta (e^{\kappa t} - 1) + \sigma \int_{0}^{t} e^{\kappa s}\sqrt{r_s} dB_s \\ e^{\kappa t} r_t &= r_0 + \theta (e^{\kappa t} - 1) + \sigma \int_{0}^{t} e^{\kappa s}\sqrt{r_s} dB_s \\ r_t &= r_0 e^{-\kappa t} + \theta (1 - e^{-\kappa t}) + \sigma \int_{0}^{t} e^{-\kappa (t-s)}\sqrt{r_s} dB_s \end{align*}\]

The mean is given by:

\[\begin{align*} \mathbf{E}[r_t] &= r_0 e^{-\kappa t} + \theta (1 - e^{-\kappa t}) \end{align*}\]

The random variable \(\sigma \int_{0}^{t} e^{-\kappa (t-s)}\sqrt{r_s} dB_s\) has mean \(0\) and variance:

\[\begin{align*} \mathbf{E}\left[\left(\sigma \int_{0}^{t} e^{-\kappa (t-s)}\sqrt{r_s} dB_s\right)^2\right] &= \sigma^2 \int_{0}^{t}e^{-2\kappa(t-s)} \mathbf{E}[r_s] ds \\ &= \sigma^2 e^{-2\kappa t}\int_{0}^{t}e^{2\kappa s} \left(r_0 e^{-\kappa s} + \theta(1-e^{-\kappa s})\right) ds\\ &= \sigma^2 r_0 e^{-2\kappa t} \int_{0}^{t} e^{\kappa s} ds + \sigma^2 \theta e^{-2\kappa t} \int_{0}^{t}(e^{2\kappa s}-e^{\kappa s}) ds \\ &= \sigma^2 r_0 e^{-2\kappa t} \left[\frac{e^{\kappa s}}{\kappa} \right]_{0}^{t} +\sigma^2 \theta e^{-2\kappa t} \left[\frac{e^{2\kappa s}}{2\kappa} - \frac{e^{\kappa s}}{\kappa}\right]_{0}^{t}\\ &= \frac{\sigma^2 r_0}{\kappa} e^{-2\kappa t} (e^{\kappa t} - 1)+\sigma^2 \theta e^{-2\kappa t} \left[\frac{e^{2\kappa s}}{2\kappa} - \frac{2e^{\kappa s}}{2\kappa}\right]_{0}^{t}\\ &= \frac{\sigma^2 r_0}{\kappa} e^{-2\kappa t}(e^{\kappa t} - 1)+\frac{\sigma^2 \theta}{2\kappa} e^{-2\kappa t}(e^{2\kappa t} - 2e^{\kappa t} - (1 - 2))\\ &= \frac{\sigma^2 r_0}{\kappa} e^{-2\kappa t}(e^{\kappa t} - 1)+\frac{\sigma^2 \theta}{2\kappa}e^{-2\kappa t} (1 + e^{2\kappa t} - 2e^{\kappa t})\\ &= \frac{\sigma^2 r_0}{\kappa} (e^{-\kappa t} - e^{-2\kappa t})+\frac{\sigma^2 \theta}{2\kappa} (1 - e^{-\kappa t})^2 \end{align*}\]

Naive python implementation

CIRProcess class

The class CIRProcess is designed as an engine to generate sample paths of the CIR process.

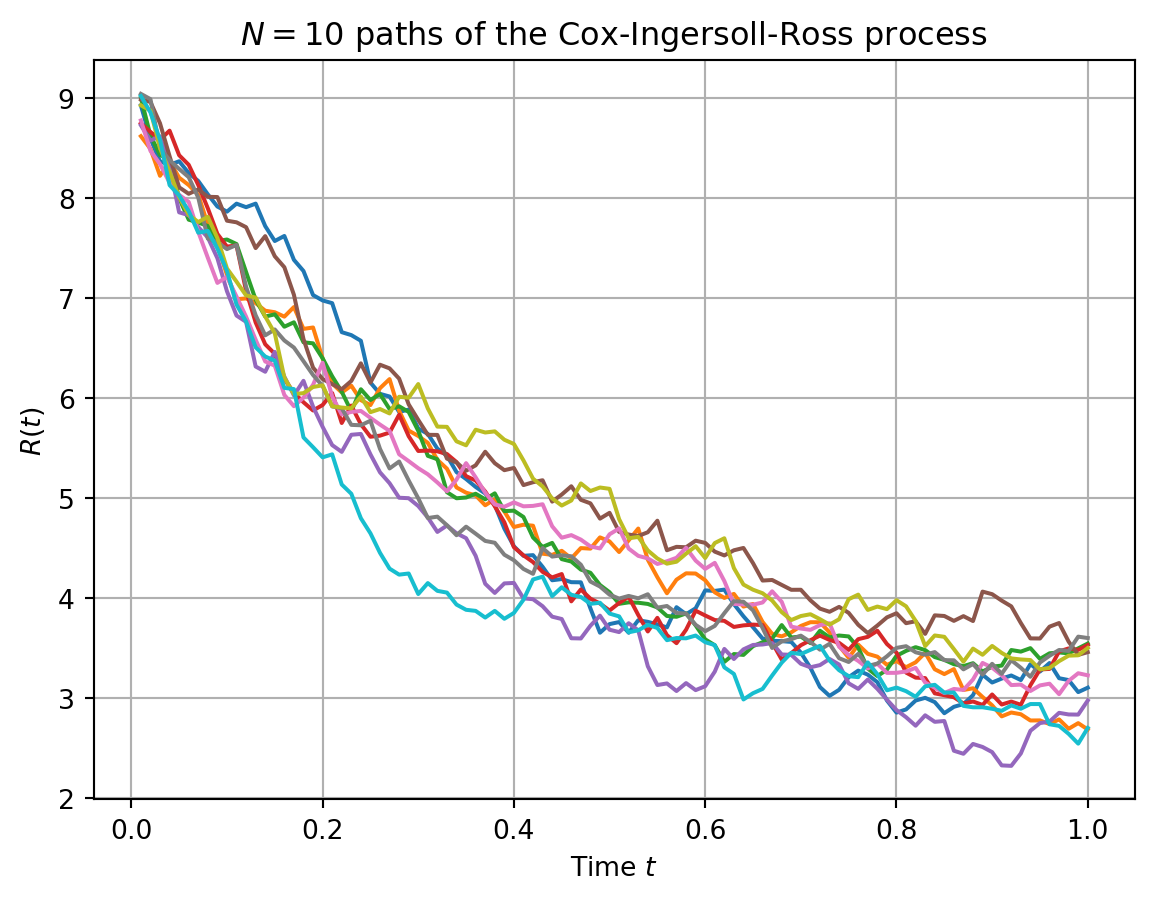

Sample Paths

We generate \(N=10\) paths of the CIR process.

Show the code

cir_process = CIRProcess(

kappa=3,

r_0=9,

sigma=0.5,

step_size=10e-3,

theta=3,

total_time=1.0,

)

num_paths = 10

paths = cir_process.generate_paths(num_paths)

t = np.linspace(0.01, 1.0, 100)

plt.grid(True)

plt.xlabel(r"Time $t$")

plt.ylabel(r"$R(t)$")

plt.title(r"$N=10$ paths of the Cox-Ingersoll-Ross process")

for path in paths:

plt.plot(t, path)

plt.show()

Evolution of the distribution.

The evolution of the distribution with time can be visualized.

Show the code

# TODO: - this is where slowness lies, generating paths is a brezze

# Wrap the paths 2d-array in a dataframe

paths_tr = paths.transpose()

# Take 20 samples at times t=0.05, 0.10, 0.15, ..., 1.0 along each path

samples = paths_tr[4::5]

# Reshape in a 1d column-vector

samples_arr = samples.reshape(num_paths * 20)

samples_df = pd.DataFrame(samples_arr, columns=["values"])

samples_df["time"] = [

"t=" + str((int(i / num_paths) + 1) / 20) for i in range(num_paths * 20)

]

# TODO: end

fig, ax = joypy.joyplot(

samples_df,

by="time",

colormap=cm.autumn_r,

column="values",

grid="y",

kind="kde",

range_style="own",

tails=10e-3,

)

plt.vlines(

[cir_process.theta, cir_process.r_0],

-0.2,

1,

color="k",

linestyles="dashed",

)

plt.show()